5 Financial Mistakes Small Businesses Can't Afford to Make

Starting and running a small business can be both challenging and rewarding. One of the key factors in ensuring its success is managing the finances effectively. Unfortunately, many small businesses make common financial mistakes that they simply cannot afford to make. In order to avoid these pitfalls, it is important for entrepreneurs to be aware of them and take proactive steps towards mitigating their impact.

1. Neglecting Regular Bookkeeping

Accurate bookkeeping is the foundation of any successful business. Failing to keep track of your income and expenses can lead to serious financial consequences down the line. Small businesses must establish a system for maintaining regular records, including sales, purchases, payroll, and tax obligations. By neglecting proper bookkeeping practices, business owners risk losing sight of their cash flow position, making it difficult to identify potential issues or opportunities for growth.

2. Overlooking Cash Flow Management

Cash flow management is vital for small businesses as it directly impacts day-to-day operations. Many entrepreneurs face challenges due to poor cash flow management which can result in liquidity problems or even bankruptcy. It is essential to closely monitor accounts receivable and payable, regularly review budget forecasts, negotiate favorable payment terms with suppliers if possible, and maintain sufficient working capital reserves.

3. Failing to Create a Realistic Budget

Without a well-defined budget plan in place, small businesses may find themselves overspending or allocating resources inefficiently - putting unnecessary strain on their finances. A realistic budget helps ensure disciplined spending while allowing room for investment in growth areas crucial for long-term success.

4. Ignoring Tax Obligations

Tax compliance should never be taken lightly by any business owner - especially when it comes to small enterprises operating within strict budgets where non-compliance penalties could have severe consequences on profitability or reputation. Keeping up with tax obligations requires staying informed about tax laws, maintaining accurate financial records, and timely filing of returns. Seeking professional advice from a qualified accountant or tax consultant may be worthwhile to navigate the complexities of taxation.

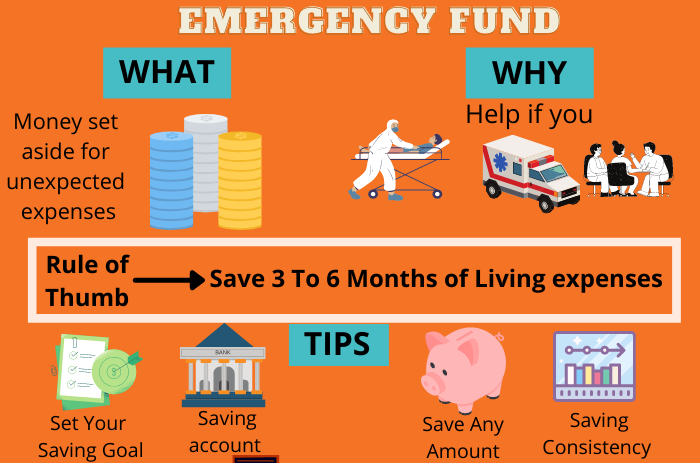

5. Lacking Emergency Funds

Unforeseen circumstances can arise at any moment, impacting a small business's stability. It is crucial for entrepreneurs to set aside emergency funds as a buffer against unexpected expenses or fluctuations in revenue. Failing to establish such reserves could lead to borrowing at unfavorable terms or even closing down operations during difficult times.

Final Thoughts

Small businesses must navigate various financial challenges while striving for growth and success. By avoiding these five common mistakes - neglecting regular bookkeeping, overlooking cash flow management, failing to create a realistic budget plan, ignoring tax obligations, and lacking emergency funds - entrepreneurs can significantly increase their chances of long-term viability and profitability. Prioritizing sound financial practices enables small businesses to make informed decisions, adapt quickly to changing market conditions, and ultimately achieve their goals.

Related Posts...