Secured vs. Unsecured Loans: Finding the Best Fit for You

When it comes to financing options, understanding the differences between secured and unsecured loans is essential in making informed decisions about your financial future. Both types of loans can serve various purposes, such as funding a new car purchase, home renovations, or covering unexpected expenses. However, there are crucial distinctions between these loan types regarding collateral requirements, interest rates, repayment terms, and overall risk involved.

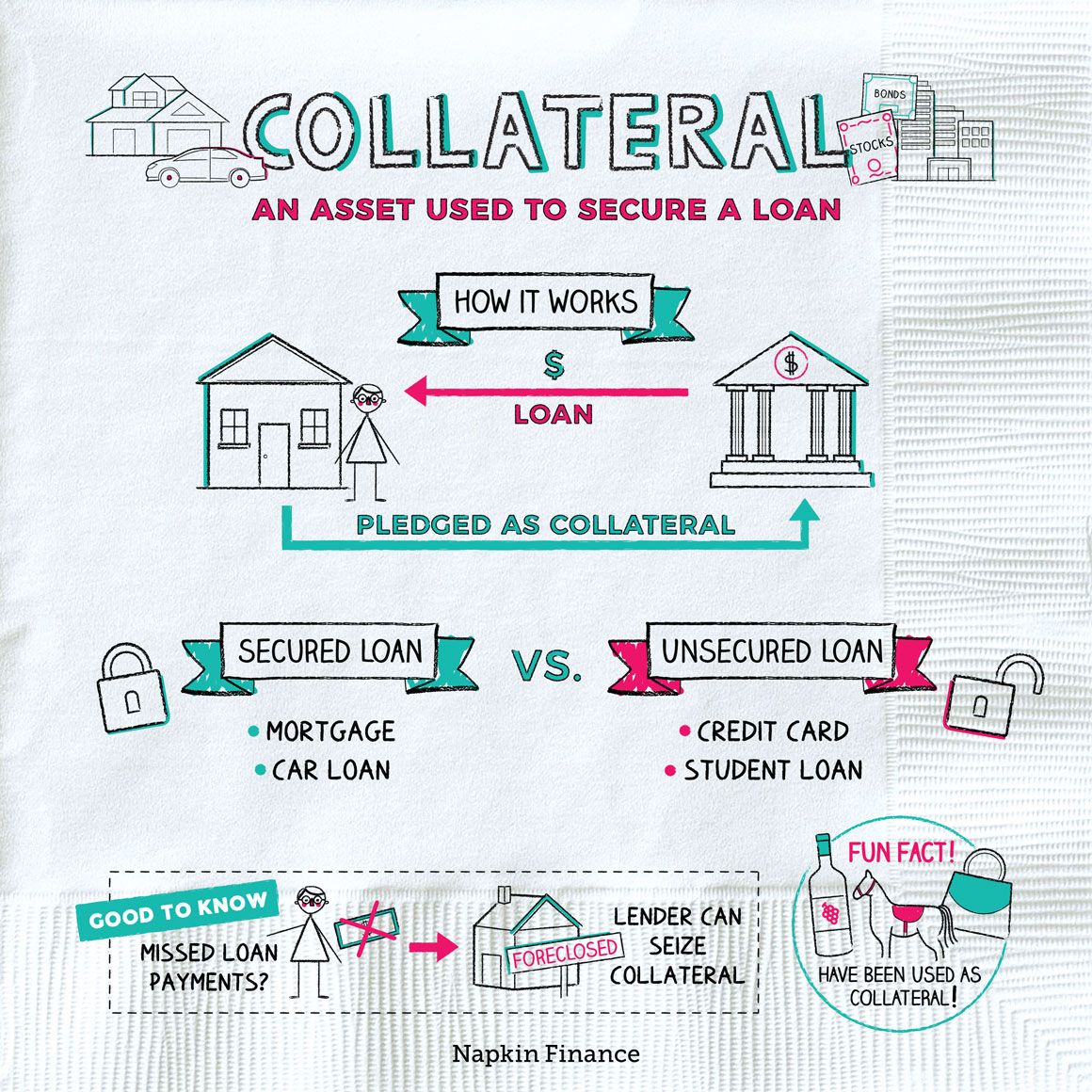

Collateral Requirements

One of the primary contrasts between secured and unsecured loans lies in their collateral requirements. A secured loan necessitates providing collateral – typically in the form of assets like real estate or vehicles – which acts as security for the lender against potential default by the borrower. This collateral provides lenders with reassurance on recovering their investment should any repayment issues arise.

On the other hand, unsecured loans do not require any form of collateral. These loans rely solely on a borrower's creditworthiness and financial history to determine eligibility and lending terms. Without requiring specific assets as guarantees, unsecured loans offer more flexibility but often come with additional scrutiny from lenders due to increased risk factors.

Interest Rates

Interest rates play a significant role when choosing between secured and unsecured loans since they directly impact borrowing costs over time. Generally speaking, secured loans tend to carry lower interest rates compared to their unsecured counterparts due to reduced risk for lenders.

Secured loan borrowers benefit from lower interest rates because if they fail to repay their debt obligations according to agreed-upon terms, lenders have recourse through seizing and selling off the pledged collateral. This added layer of protection allows lenders greater confidence in extending favorable interest rates.

Unsecured loan borrowers face higher interest rates since these loans lack tangible assets backing them up. Lenders compensate for increased risk by charging higher interest fees as a way to mitigate potential losses if borrowers default on payments.

Repayment Terms

Repayment terms can also differ significantly between secured and unsecured loans. Secured loans often offer longer repayment periods, which can range from several years to decades, depending on the loan amount and purpose. This prolonged duration allows borrowers greater flexibility in managing their monthly payments, making it easier to fit within their budgetary constraints.

Unsecured loans typically come with shorter repayment terms due to increased risk exposure for lenders. These loans generally have fixed time frames ranging from a few months to a few years. While the shorter term may mean higher monthly payments, it does provide borrowers with the advantage of completing loan repayments more quickly and potentially reducing overall interest paid over time.

Overall Risk Involved

When assessing secured versus unsecured loans, understanding the associated risks is crucial for making informed decisions tailored to your financial circumstances. As previously mentioned, lenders face less risk when offering secured loans since they can repossess collateral if borrowers default on payment obligations. This lower level of risk allows lenders to be more lenient regarding credit history requirements and often results in better loan terms for borrowers.

On the contrary, unsecured loans pose higher risks for lenders as there is no specific asset or collateral securing these debts. Lenders rely heavily on borrower creditworthiness as an indicator of future repayment capabilities. Consequently, obtaining approval for unsecured loans tends to require stronger credit scores and stable income streams while offering slightly less favorable lending terms compared to secured options.

Final Thoughts

Choosing between secured and unsecured loans depends on various factors such as personal preferences, financial stability, borrowing needs, and long-term goals. Secured loans provide lower interest rates but necessitate collateral as security against potential defaults; whereas unsecured loans do not require assets but carry higher interest rates due to increased lender risk.

It's essential always to consider your current financial situation before committing yourself to any form of borrowing arrangement diligently. The decision should align with your ability to manage monthly payments comfortably and achieve your financial objectives while minimizing unnecessary risks. By understanding the differences between secured and unsecured loans, finding the best fit for your specific needs becomes a more manageable task.

Also Read...