How Can You Qualify for a Secured or Unsecured Loan?

When it comes to obtaining financial assistance, many individuals turn to loans as a viable option. Loans provide the much-needed funds to meet various personal and business needs. However, before applying for a loan, it is important to understand the two main types of loans available: secured and unsecured.

Secured and unsecured loans differ in terms of collateral requirements and risk levels for lenders. In order to qualify for either type of loan, there are certain factors borrowers must consider.

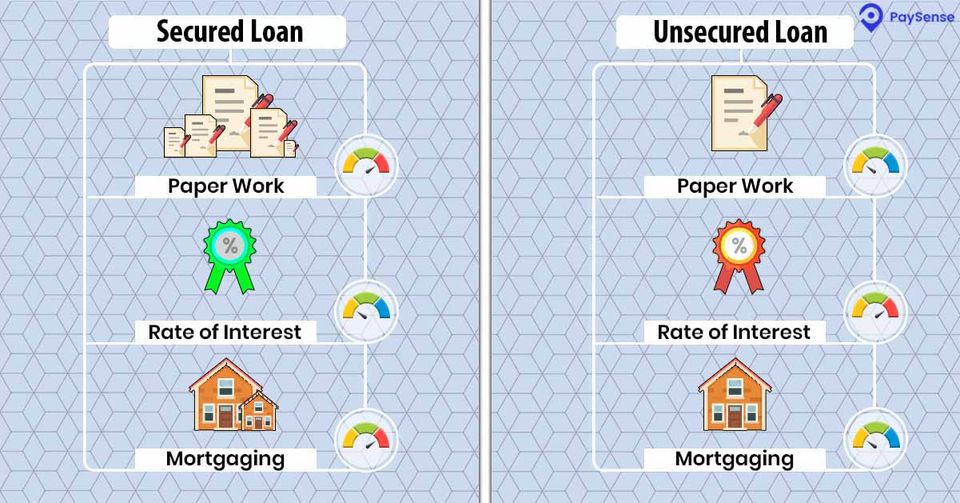

Secured Loans

A secured loan requires borrowers to provide collateral as security against the borrowed amount. This collateral can be in the form of assets such as real estate properties, vehicles, or valuable possessions. By offering collateral, borrowers reduce the risk perceived by lenders when granting them funds.

Creditworthiness

Although secured loans have lower credit score requirements compared to unsecured loans due to the presence of collateral, creditworthiness still plays a significant role in qualifying for such loans. Lenders typically assess applicants' credit scores and payment histories during their evaluation process.

Collateral Evaluation

The value and equity of the offered collateral play a crucial role in determining loan eligibility. Lenders will evaluate these factors alongside other considerations like current market conditions and potential risks associated with accepting particular types of assets as collaterals.

Income Verification

Having a stable income is vital when applying for a secured loan. Lenders need assurance regarding your ability to repay the borrowed amount within agreed-upon terms. Providing proof of consistent income through employment letters or bank statements assists lenders in assessing your repayment capability.

Unsecured Loans

Unlike secured loans, unsecured loans do not require any form of collateral from borrowers. Instead, lenders evaluate applicants based on their creditworthiness alone since they bear higher risks without any asset backing.

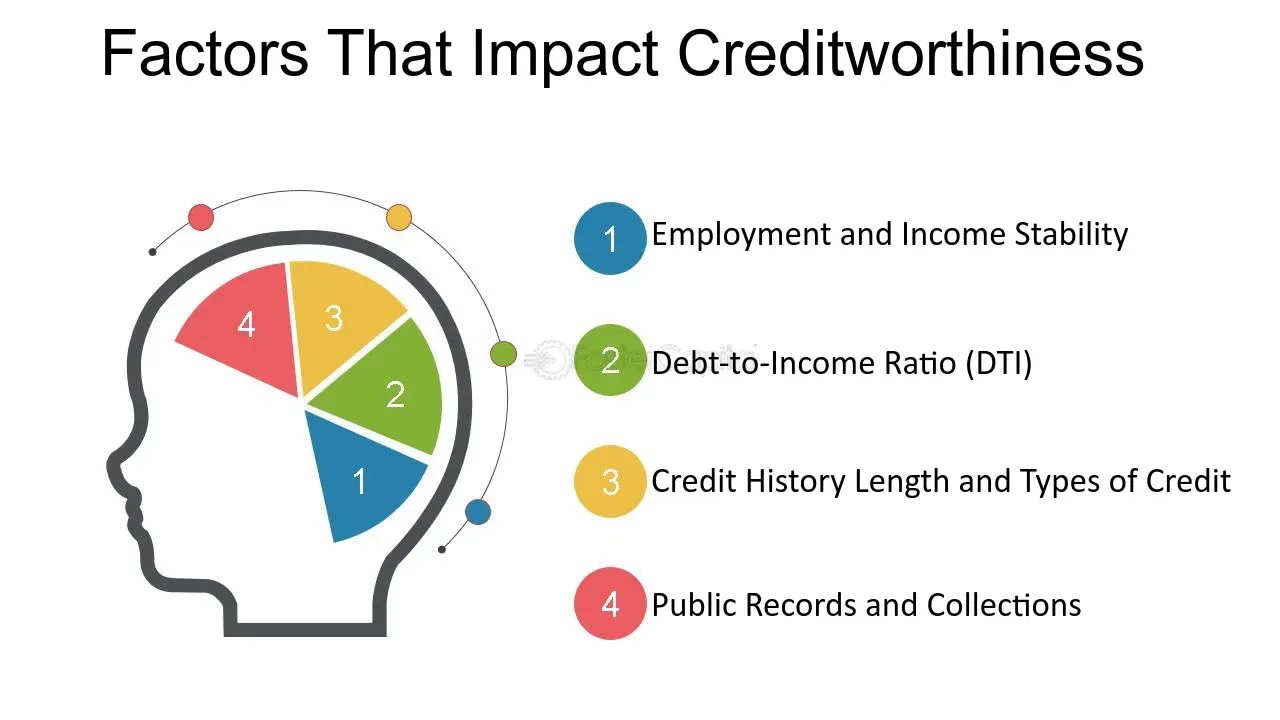

Credit Score Importance

Credit scores play a critical role in determining eligibility for unsecured loans because lenders rely heavily on these scores to assess borrowers' creditworthiness. A higher credit score indicates a more favorable financial history, increasing the likelihood of loan approval.

Debt-to-Income Ratio

Lenders also consider the debt-to-income ratio (DTI) when evaluating unsecured loan applications. DTI is calculated by dividing monthly debt payments by gross monthly income. A lower DTI suggests better financial stability and increases the chances of securing unsecured loans.

Employment Stability

Having a stable employment history can positively impact your eligibility for unsecured loans. Lenders view steady employment as indicative of reliable income, increasing confidence in your ability to repay borrowed funds.

To Wind Up

Qualifying for either a secured or unsecured loan requires careful consideration of various factors. For secured loans, collateral evaluation, creditworthiness, and stable income verification play significant roles in obtaining approval. On the other hand, for unsecured loans, credit scores, debt-to-income ratios, and employment stability carry greater weight during the evaluation process.

Understanding these requirements will help borrowers determine which type of loan suits their needs best and enable them to prepare necessary documentation accordingly. By meeting eligibility criteria set forth by lenders for both types of loans, individuals can increase their chances of successfully obtaining much-needed financial assistance while managing associated risks effectively.

Related Stories...